When it comes time to turn a lifetime of diligent savings into cash flow to help fund your retirement years, you’ll want to know your money is managed conservatively without giving up on the prospect of long-term growth that offsets inflation. A cash wedge strategy can help you achieve these goals.

With a cash wedge strategy, you can:

- Withdraw cash flow from a conservative investment to help maintain your current lifestyle.

- Continue to grow your retirement nest egg to provide ongoing growth potential.

- Maintain your peace of mind knowing you can access your money when you need it.

Here's how it works:

- Allocate 1-3 year’s worth of cash flow to a “cash wedge” - typically a low risk investment such as the Counsel High Interest Savings Fund. The remainder of your savings is invested in a balanced solution like the Counsel Global Income & Growth Portfolio to help provide cash flow and long term growth.

- Next, your advisor sets up a systematic withdrawal plan that can provide you with regular monthly payments from the cash wedge.

- As you withdraw regular monthly payments, the cash wedge may replenish with any potential distributions from the Counsel Global Income & Growth Portfolio to help you keep 1-3 years worth of cash flow in a conservative investment.(1)

Advantages of a Cash Wedge Strategy:

- Sets aside 1-3 years of cash flow in a solution that is not subject to market volatility (e.g. High Interest Savings Fund).

- Once set up, it runs automatically to provide steady cash flow to you.

Two Solutions Working Together to Help Provide Cash Flow

Counsel High-Interest Savings Fund for Your Cash Wedge

The Counsel High Interest Savings Fund invests primarily in high interest deposit accounts, which provides it with a competitive interest rate on cash balances.(2) It is a low-risk investment solution designed to help meet your short term cash flow requirements and offers a compelling alternative to a traditional savings account or Guaranteed Investment Certificates (GICs).(3)

With the flexibility to withdraw your money at any time, the Counsel High Interest Savings Fund is an ideal investment to help deliver regular monthly cash flow from a cash-wedge strategy.

Counsel Global Income & Growth Portfolio for your Global Equity Balanced Solution

With changes in interest rates leading to volatility in the stock markets, you need a well-diversified solution that can provide cash flow from multiple sources along with total return potential. For the core of your cash wedge strategy, consider Counsel Global Income & Growth Portfolio to provide you with those diversified sources of return and the potential for long-term growth:

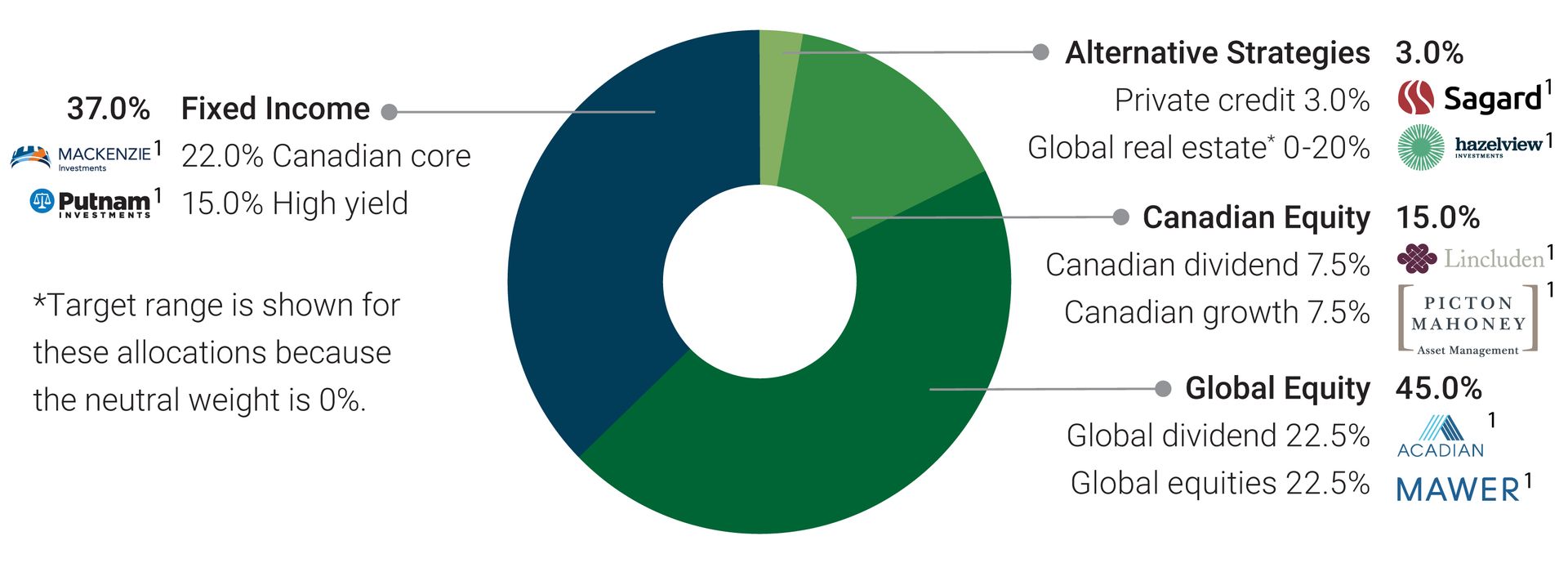

- A blend of equities, fixed income, and alternative assets to help provide diversified return sources through price growth and income generation.

- Multiple sources of cash flow that include Canadian and global dividends, higher-yielding fixed income, global real estate, and liquid alternatives.

- Concentrated equity strategies for growth to to help your long-term capital continue to grow to offset inflation.

The asset allocation weights depicted above represent the target allocations for the fund and may differ from the current allocation. The target allocation may comprise a combination of investments in equities, fixed income securities, securities that are designed to track a market index or other securities. Canada Life Investment Management Ltd., the portfolio manager of the fund, has the discretion to change the allocation without prior notice.1 Firms listed are sub-advisor or manager of the underlying funds. For further information on the underlying funds, please see the investment objectives and strategies in their simplified prospectus or fund facts.

Minimize Your Retirement Income Risk

Implementing a cash wedge strategy by combining a long-term solution, such as the Counsel Global Income & Growth Portfolio, with the Counsel High Interest Savings Fund, can help you minimize the effects of short-term market volatility helping to ensure your longer-term funds can still grow for the future.

Call your advisor today to learn how implementing a cash wedge strategy can help you achieve your long-term investment goals.

(1) The payment of distributions is not guaranteed and may fluctuate. The payment of distributions should not be confused with a fund’s performance, rate of return or yield. If distributions paid by the fund are greater than the performance of the fund, your original investment will shrink. Distributions paid as a result of capital gains realized by a fund, and income and dividends earned by a fund, are taxable in your hands in the year they are paid. Your adjusted cost base will be reduced by the amount of any returns of capital. If your adjusted cost base goes below zero, you will have to pay capital gains tax on the amount below zero.

(2) Interest is calculated daily on the total closing balance in the Fund’s investments on each day and paid monthly. The effective interest rate paid to unitholders may vary from the gross rate provided to the Fund depending on multiple factors including the fees of the series purchased, the settlement date of the purchase and the growth rate of the fund.

(3) Unlike mutual funds, the returns and principal of GICs are guaranteed.

The views expressed in this commentary are those of Canada Life Investment Management as at the date of publication and are subject to change without notice. Prospective investors should review the offering documents relating to any investment carefully before making an investment decision and should ask their advisor for advice based on their specific circumstances. The content of this material (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

Commissions, trailing commissions, management fees, and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual fund securities are not covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer. There can be no assurances that the fund will be able to maintain its net asset value per security at a constant amount or that the full amount of your investment in the fund will be returned to you. Past performance may not be repeated.

Counsel Portfolios are managed by Canada Life Investment Management Ltd. Counsel Portfolios are distributed by Quadrus Investment Services Ltd., IPC Investment Corporation, and IPC Securities Corporation, and may also be available through other authorized dealers in Canada. Investment Planning Counsel is a fully integrated wealth management company.

Trademarks owned by Investment Planning Counsel Inc. and licensed to its subsidiary corporations.